Image Source: Big-Dividend REITs, NosUA/iStock via Getty Images

Image Source: Big-Dividend REITs, NosUA/iStock via Getty Images

Realty Income, also known as the monthly dividend company, has proven to be a safe haven for investors during these uncertain times. While markets have experienced sharp declines, Realty Income's share price has actually seen an increase. However, investors are now questioning whether Realty Income still offers an attractive valuation or if it's time to explore other investment options. In this article, we will discuss the relative attractiveness of Realty Income's shares, including their business strategy, risks, and current valuation compared to other big-dividend REITs and dividend aristocrats.

Overview:

Realty Income Corp (NYSE:O) was founded in 1969 and went public in 1994. The company's core focus is on acquiring and managing commercial real estate properties. Realty Income's impressive track record of dividend increases has earned it a spot among the elite group of S&P 500 Dividend Aristocrats. These are companies that have consistently increased their dividends for at least 25 consecutive years. With over 6,700 properties in its portfolio, Realty Income generates rental revenue from long-term lease agreements with commercial tenants, including major names like Walgreens, CVS, and Dollar Tree.

Image Source: Realty Income Investor Presentation

Image Source: Realty Income Investor Presentation

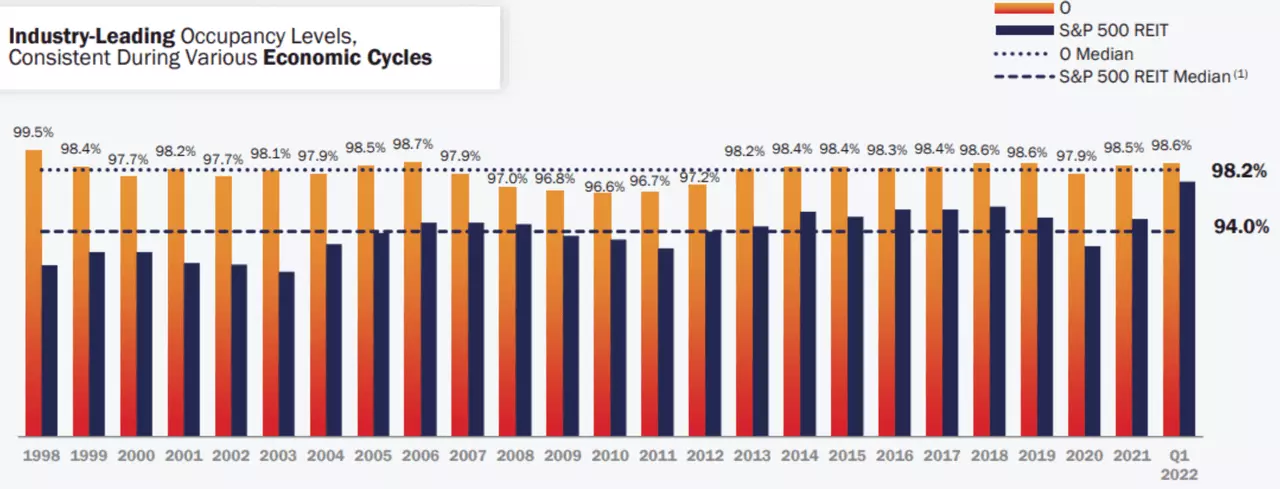

The company's portfolio is highly diversified across tenants, industries, and geographies. Nearly 96% of its rental revenue comes from tenants with a nondiscretionary service and/or a low price point component to their business. This makes Realty Income's tenants resilient to economic downturns and less susceptible to e-commerce pressures.

Business Strategy:

As one of the most stable and financially strong REITs in its space, Realty Income sees acquisitions as a significant part of its growth strategy. The company has the financial strength to pursue this strategy, with two A3/A- ratings, making it one of only seven U.S. REITs to achieve such high ratings. The current market conditions, combined with potential distress in the wake of economic challenges, create an attractive environment for Realty Income to pursue acquisitions.

One notable recent merger was with VEREIT, which allowed Realty Income to enhance its size and scale as a premier net lease REIT, consolidating a highly fragmented net lease industry.

Risks:

While Realty Income has proven to be a stable and financially strong company, it still faces risks. One challenge is its already substantial size, which can make it difficult to achieve significant growth at scale. Another risk is the potential impact of rising interest rates. While Realty Income has long-term leases with built-in rent escalators, high inflation could put pressure on margins. However, as the company continues to acquire new properties, rental rates are likely to align with market rates over time.

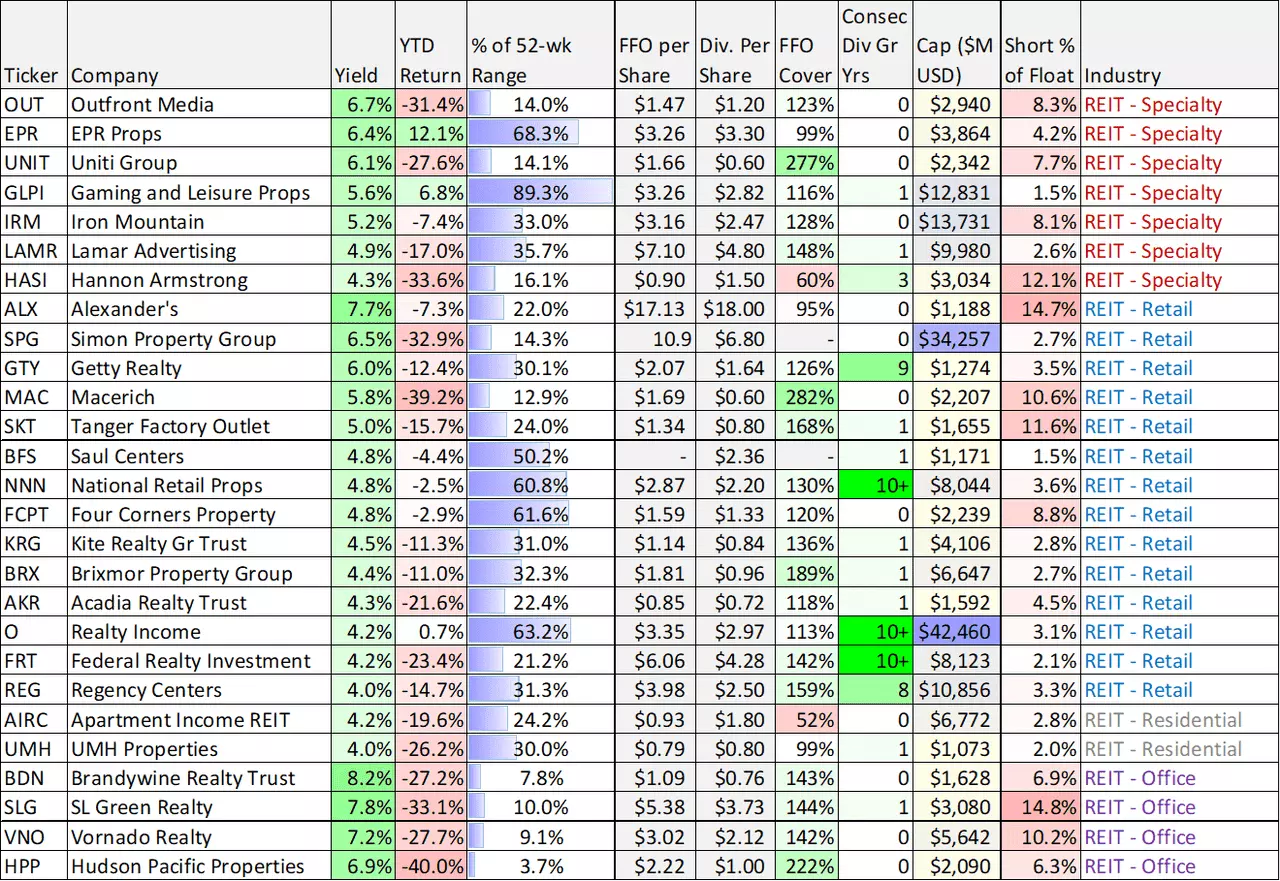

50 Big-Dividend REITs, Compared:

Image Source: blueharbinger.com, data as of 21-Jul-22

Image Source: blueharbinger.com, data as of 21-Jul-22

To provide further insight into Realty Income's performance, let's take a look at some important metrics comparing it to 50 other big-dividend REITs. While most REITs have experienced significant declines this year, Realty Income has bucked the trend. This can be attributed to its stability in times of volatility.

Valuation:

From a valuation perspective, Realty Income may appear relatively expensive compared to some peers. However, this higher valuation is a result of its stronger and healthier business, as well as its outperformance in the market. Realty Income's price-to-Adjusted-FFO multiple is higher than many of its peers because it carries less risk. Despite being considered relatively expensive, Realty Income still has positive expected growth in Adjusted Funds From Operations (AFFO) for this year and the next. As the company continues to grow its acquisition pipeline, the expected growth for 2023 is likely to increase.

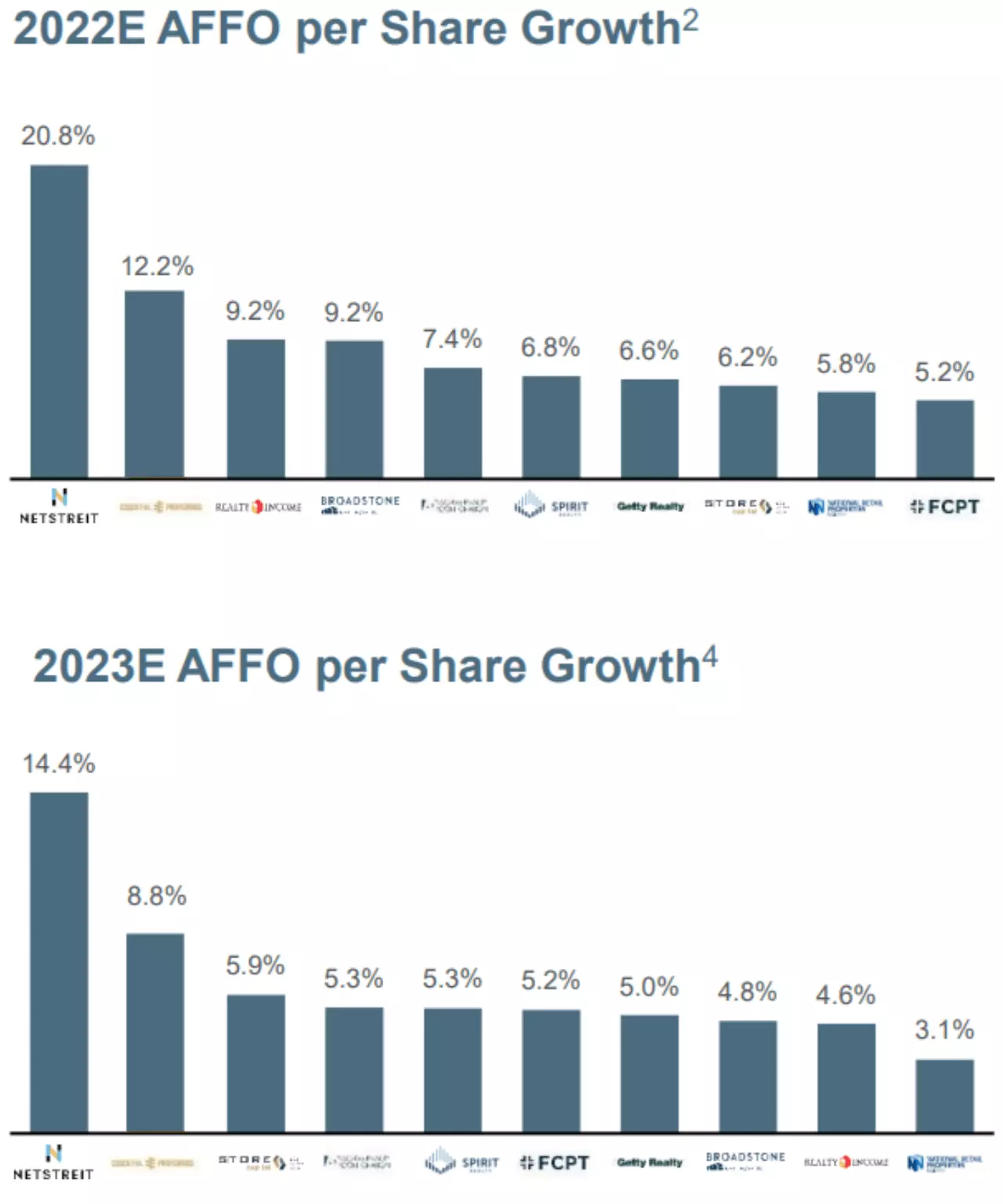

Image Source: Essential Properties Realty Trust ((EPRT)) Investor Presentation

Image Source: Essential Properties Realty Trust ((EPRT)) Investor Presentation

Furthermore, Realty Income's valuation remains attractive by historical standards. The company's FFO per share exceeds pre-pandemic levels, yet its share price does not. This indicates that Realty Income currently trades at an attractive price-to-FFO multiple.

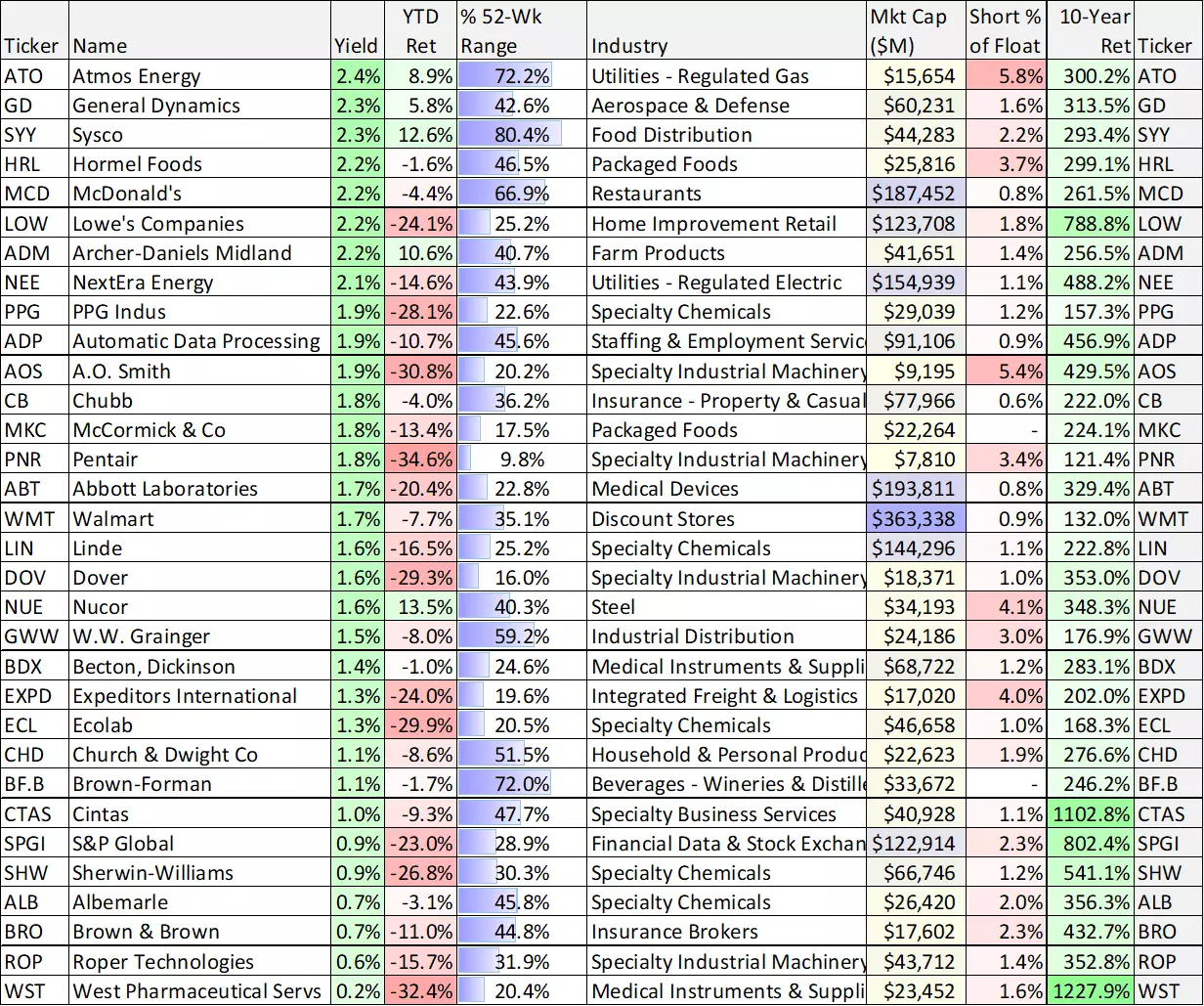

Realty Income Versus Dividend Aristocrats:

Comparing Realty Income to its dividend aristocrat peers, which are S&P 500 companies that have increased their dividends for at least 25 consecutive years, provides valuable insights. Realty Income not only has the 6th highest dividend yield among these peers but has also delivered a positive total return this year. This demonstrates the company's stability during times of market volatility.

Image Source: blueharbinger.com, data as of 21-Jul-22

Image Source: blueharbinger.com, data as of 21-Jul-22

It is important to note that companies with the best 10-year performance often have the lowest dividend yields. This serves as a reminder not to chase after stocks solely based on high dividend yields. Realty Income has managed to deliver a respectable 10-year return while maintaining a strong dividend that is well covered by funds from operations.

The Bottom Line:

In summary, Realty Income remains an attractive investment opportunity for investors seeking steady income growth and potential price appreciation. The company's strong financial position, prudent acquisition-focused strategy, robust dividend growth, and attractive valuation make it stand out in the market. Additionally, its portfolio of prime location properties offers stability in the face of the online shopping trend. Despite the risks, such as rising interest rates and conservative rent escalators, Realty Income continues to present an enticing opportunity. As long-term contrarians, we are confident in the company's potential and remain invested in Realty Income, along with other attractive REITs, in our Income Equity portfolio.